The Dow Average has been anything but average recently. In fact, the S&P 500 has consistently outperformed it over the last one, two, five, and ten-year periods. That makes the Dow Jones Industrial Average a below-average portfolio.

What’s the problem?

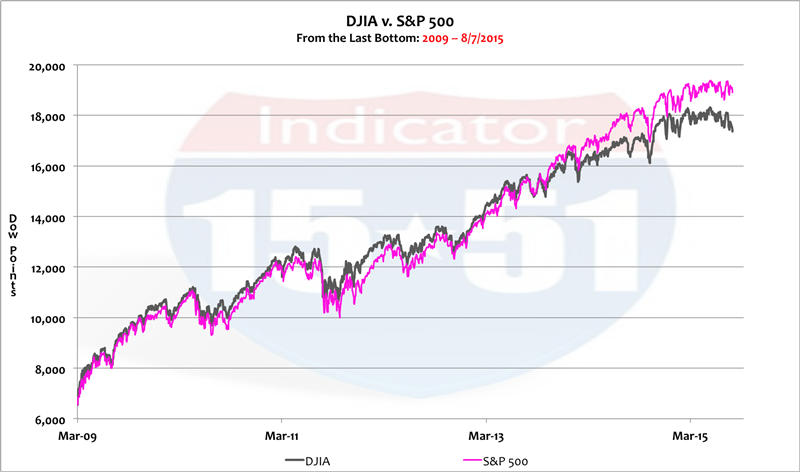

Perhaps the greatest benefit of a small portfolio is its ability to turnaround quickly and provide rapid growth after corrections. As such, one would expect the Dow 30 to have greatly outperformed the 500 stocks of the S&P since the bottom of the last correction (March 2009). But that hasn’t happen. See below.

During this six-plus-year period the S&P outperformed the Dow by 23 percentage points (189% versus 165%), or 4% per year. That’s absurd.

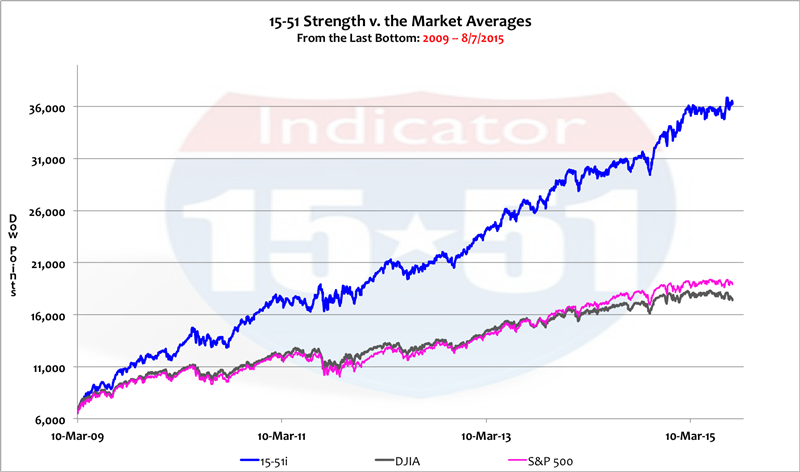

A 500 stock index should never consistently outperform a 30 stock portfolio. Never. Instead, the Dow’s performance should have been somewhere between the S&P 500 and the 15-51 Indicator (see below.)

The Dow, right now, should be somewhere over 21,000. Not only can it not get there, but it also can’t beat the S&P 500. Why?

The DJIA has structural issues, and more specifically, suffers from poor stock selection. Think of this…

Of the Dow’s 30 components only 12 have outpaced the S&P 500 over the last year – and one-third of those are financial stocks (Goldman Sachs, Visa, Travelers Insurance Group, and JP Morgan Chase). In fact, the Dow currently has five financial stocks, which ranks that industry 4th in priority order. But because the financial industry accounts for the majority of the Dow’s gains, such an allocation signifies that the financial industry contributes 1/3 of all economic growth in America. That isn’t even close to being accurate indication.

The Dow’s highest ranked industry is technology, with 7 stocks that amount to approximately 23% of the entire Dow portfolio – and 5 of those seven stocks have underperformed the S&P by huge amounts (IBM, United Technologies, Microsoft, Intel, and Cisco Systems). As stated in my book, technology is about the future – and much of those five Dow tech-stocks are about the past. This industry clearly needs some updating.

In the Dow’s second ranked industry, consumer services, half of its components have consistently underperformed the S&P 500 (McDonalds, Wal-Mart, and Verizon) – as did 4 of the six consumer staples stocks (Coke, Johnson & Johnson, Procter & Gamble, and Merck). Needless to say, these industries also need some tender-loving care.

This is not to mention that all of the Dow’s energy and basic stocks have also failed to meet the S&P’s performance (ExxonMobil and Chevron, Caterpillar and DuPont, respectively.)

The Dow has become a pitiful collection of mediocrity, and the proverbial cherry on top is General Electric, the only original Dow component still remaining in the portfolio, which hasn’t sniffed a reasonable return since Jeff Immelt took office. He is clearly no Jack Welch.

Add them all up and a stunning 18 out of 30 stocks, or 60%, of the Dow’s components have underperformed an easy-to-beat S&P 500 index.

That’s an embarrassment.

It’s time for the people managing the Dow to make some drastic changes. It’s time to eliminate the redundancies and upgrade the portfolio’s brands and components. It’s time to put nostalgia aside and finally say goodbye to stalwart names like IBM and General Electric. Yes, they’ve been there for a long time. But who cares. Investment is a performance business – and the S&P 500 is kicking the Dow’s behind. (Again, there’s no good reason for a 500 stock index to consistently outperform a 30 stock portfolio.)

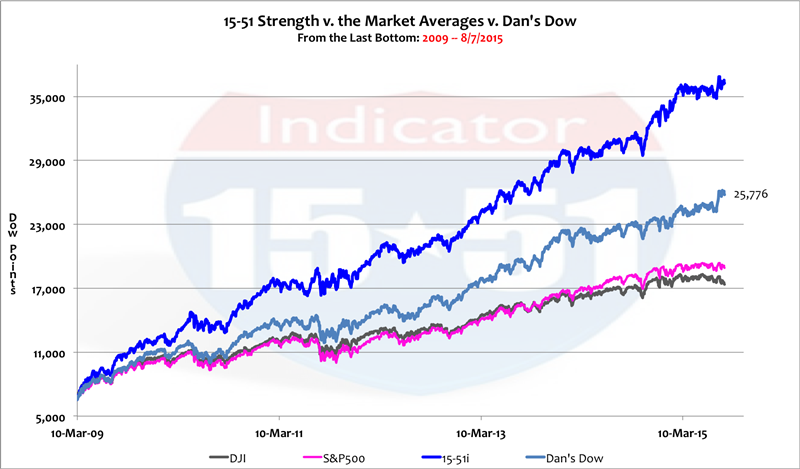

The main objective of LOSE YOUR BROKER NOT YOUR MONEY is to teach investors the art of portfolio construction and how to build a superior one. If investors understand the concepts of construction there is no portfolio on earth that they can’t fix and/or outperform. To demonstrate this I will use the techniques outlined in my book to make adjustments to the DJIA, creating in essence, my version of what the Dow should look like today.

Knowing that the Dow needs to upgrade itself to better reflect the modern day market, two technology moves are obvious – IBM and Cisco have to go. IBM will be replaced with a computer company for the modern era, Google (GOOGL), which will really bolster the personal computing segment (recall that Apple was added to the Dow earlier this year.) In addition, the Google move will make it easy to replace Cisco Systems with the multi-faceted Cummins Inc. (CMI), which would help diversify this industry by GDP spending class.

In the consumer service industry, McDonalds, Wal-Mart, and Verizon, will be replaced by companies that better reflect the changing patterns of American spenders: Panera (PNRA), Costco (COST), and amazon.com (amzn) will be added.

Consumer staple Coke will be eliminated in favor of Church & Dwight (CHD) and superior pharmaceutical developer Gilead (GILD) will replace Merck.

The financial industry is a place that the Dow can upgrade by getting smaller. For instance, with Visa and Goldman Sachs in the portfolio there’s no reason to suffer with the poor long-term performance of American Express. And as suggested earlier, the Dow currently has too many financial stocks. As a result Amex will be eliminated and not replaced.

In the industrial industry GE is out and Ford Motor Company is in, and with the extra slot created by eliminating Amex in the financial industry, conglomerate Parker-Hannifin (PH) will be added to expand this industry’s offering.

The choices the Dow’s managers have made for the energy industry is one of their most perplexing. I appreciate the wisdom of an integrated oil and gas company for the portfolio – but two of them? Having both ExxonMobil and Chevron is the epitome of redundancy. That duplication is eliminated in my version of the Dow Jones Average where Chevron gives way to Piedmont Natural Gas (PNY).

Those adjustments change 1/3 of the Dow’s components, 10 in all, and would upgrade and modernize the portfolio. And since the changes made preserved market allocations, my version of the Dow Average would remain a “market portfolio.” The portfolio’s movements will prove that should it move in a “market-like” way.

Once again, the purpose of these changes is to elevate the Dow’s performance trend to where it should be – somewhere between the S&P 500 and the 15-51 Indicator.

The chart below shows my version of the Dow Jones Industrial Average placed among the other major market indexes (the current DJIA, S&P 500, and 15-51 Indicator). See below.

The changes made almost double the Dow’s output since the last market bottom in ’09 (294% versus 189%), and places the value right where it belongs – between the S&P 500 and the 15-51 Indicator – while continuing to move in a “market-like” way.

Building and/or fixing portfolios to achieve desired results is quite easy to do using the techniques of my award winning method.

Until next time…

![]()