Volatility returned to the stock market in January 2018 and it hasn’t left, nor should it be expected to leave. It’s a function of the times and conditions. It is election year, after all. So if market instability makes you nauseous then maybe it’s time to reduce your exposure to the stock market – because it’s not going away.

Investing is not about buying at the lowest and selling at the highest. That’s a speculative view. Instead, successful investment is about buying low and selling high – to profit, according to your objectives and risk tolerances. So forget about trying to pick tops and bottoms; market timing is a gamble not worth taking.

The greatest opportunity to make the most money in stocks is buying low during major corrections, when everything is on sale and selling at discount prices. This is impossible to do if you have no dry powder, meaning your portfolio is fully invested and without the means to buy when necessary. Indeed, it’s easy to feel a burning sensation in your stomach when fully invested in markets like these.

So if you’re feeling that way trust your gut and review your investment plan and how your portfolio’s structure relates to current Market conditions. (Remember: buying low requires cash. To not have a stockpile now is a major blunder.) The analysis begins with Market conditions and that conversation starts with yields and not stocks.

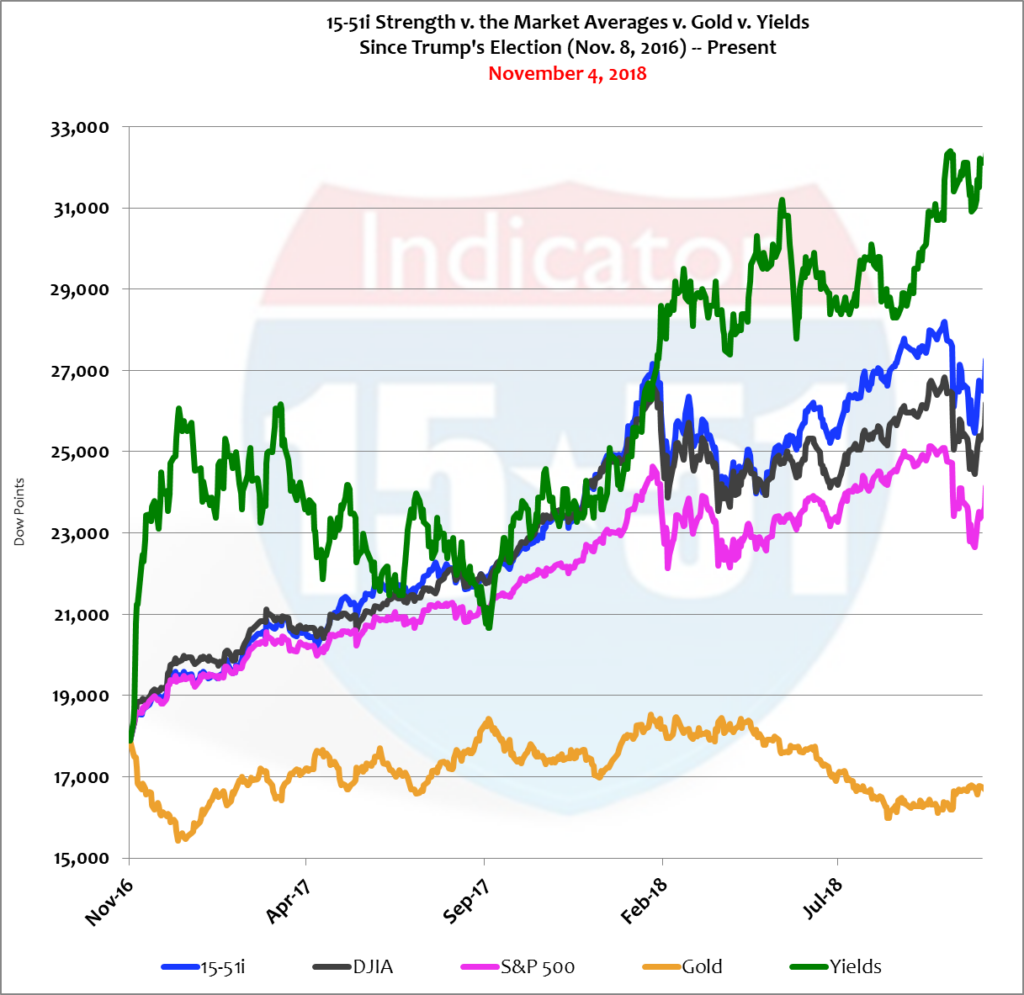

The 10-year is up 34% so far this year and has been on an upward move since Trump won the election, and with no apparent end in sight. Key Federal Reserve rates remain at historic lows, and strong employment and solid economic growth provide Chairman Powell all the ammunition needed to maintain his planned course of rate increases. Accelerated inflation will give him firepower to hasten the hikes if he so chooses. Below is a chart that spans the two years since Trump’s victory.

Yields are up 80% in the two years since the election, indicating a stronger dollar and tighter money. Gold is down fractionally (6%) in the same time, which is really a muted move compared to the increase in monetary value. It has been beaten down for years because inflation was non-existent. But that dynamic has changed, making gold low at these levels. If there is a safe place to invest outside of the U.S. dollar it is in gold.

The pace of inflation slowed a bit in the 3rd quarter versus the 2nd (from 4.1% to 3.5%) but it is poised to move higher. On October 31, 2018 the Wall Street Journal posted an article detailing how producers of things from “plane tickets to paint” are experiencing higher broad line costs and are readying to pass those increases onto consumers – who now have more money to absorb those higher prices. Wages increased by 3.1% year-over-year in October, the biggest gain since 2009.

Such a dynamic, higher prices and wages, could prompt the Federal Reserve to expedite interest rate hikes to corral inflation to support economic stability. Whatever the case, be it controlled or not, higher inflation is a major threat to stock valuations, bonds, and international economies.

Of course, inflation will push yields higher than central banks intend. The entire inflationary effect, however, is almost a complete unknown. Institutional investors hate that uncertainty. They’d much rather measured changes in rates controlled by central banks. Inflation throws a wrench into that stability, and with it comes the possibility of runaway yields – and that’s what has institutional investors so anxious.

Anxiety breeds volatility.

Interest rates run in an opposite direction as bond values. When rates rise bond values fall – and we are in a higher interest rate environment. Even though yields are up sharply in two years they are still really low. The 10-year yield is just 3.2%. It should be 6% by now. So they have a lot of room to move higher, and they will. That makes bonds richly valued at the current time.

And so are stocks – even after the most recent pullback.

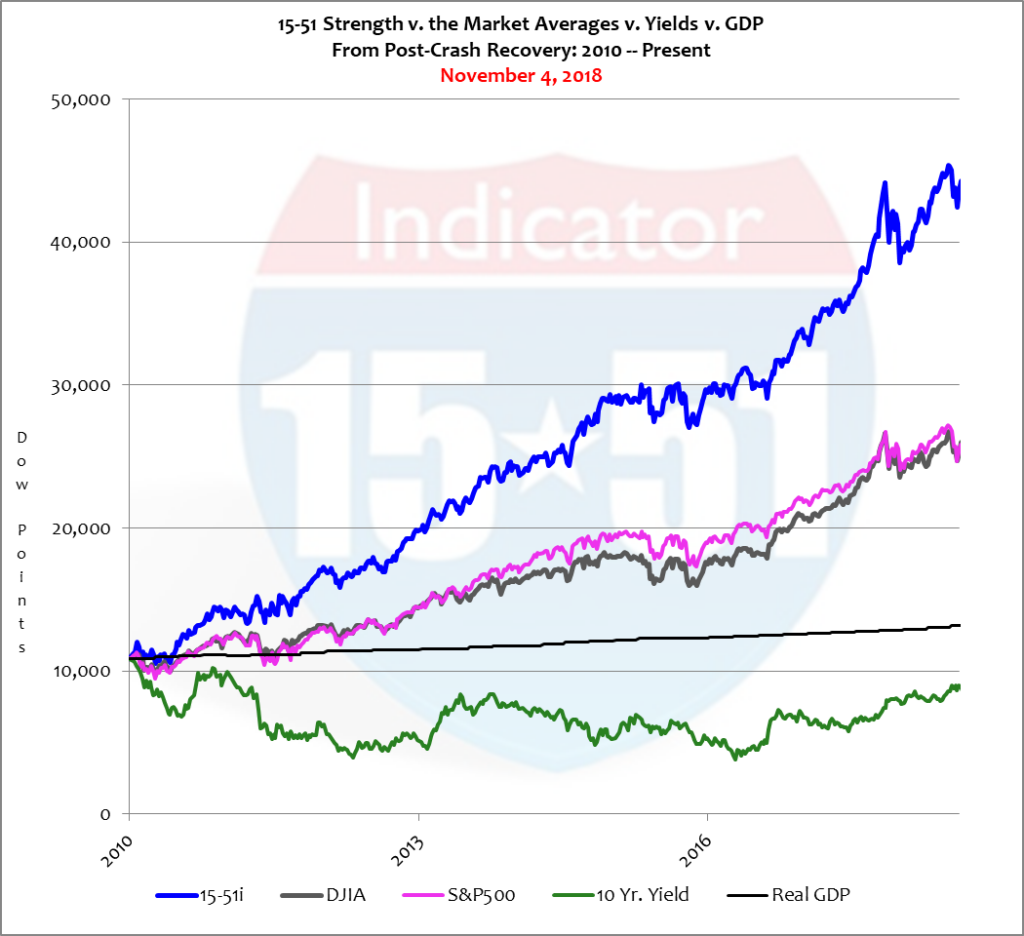

Stocks have been on an absolute tear since the economy recovered from recession in 2010, with stock market strength via the 15-51 Indicator™ gaining 303% (or 35% per year) versus a 133% advance (or 16% per year) for the Market Averages. Real economic growth was just 2.5% per year during that time. In other words, stock market gains have been inconsistent with underlying economic output for many consecutive years. That put a ton of inflation into current stock market values, which is best seen through the untainted trend-line of the 15-51 Indicator™. See below.

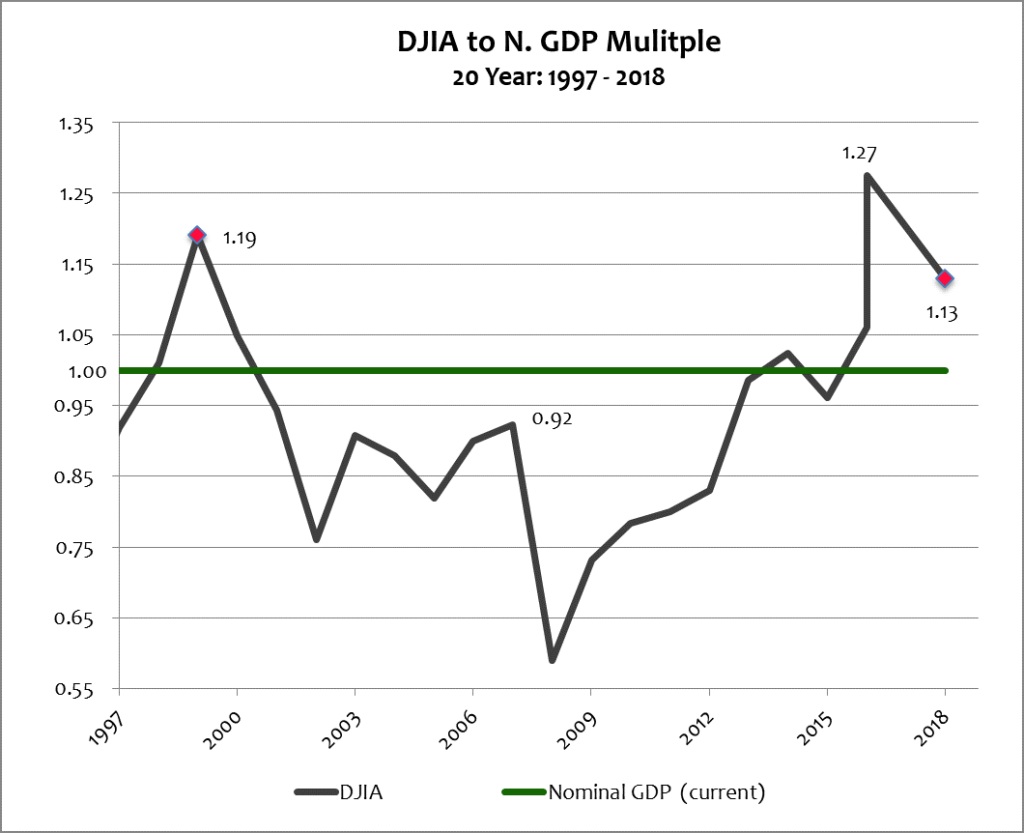

Further proof can be seen through “the market’s” multiple to GDP, which is still valued 3% higher than the tech-boom at its peak, and 33% higher than the top of the housing boom. That’s nuts. See below.

Wild swings in price do not indicate stability or consensus – two traits present in the stock market during year one of Trump’s tenure but non-existent in the second. Investors, of course, are reacting to higher interest rates and yields with the threat of higher inflation, not to mention the Trade War and the deteriorating condition overseas.

And despite President Trump’s declaration that this is the best economy in American history the numbers don’t corroborate that. At the peak of the tech-boom the economy was growing 4.7% in Real terms and unemployment was 3.8% – levels sustained for more than four years. Third quarter 2018 posted solid results, Real economic growth was 3.5% and unemployment was 3.7% – but the Trump economy has just started to hum and it’s already the end of the cycle. There’s no way it can continue like this for three more years. The world is already starting to fall apart. Speaking of which…

Have you heard that Alibaba (China’s amazon.com) cut its growth forecast by six points to 4%? That’s the world’s second largest economy. Not good. And things are much worse in weaker nations.

These conditions, highly inflationary valuations and anxiety about the future, are certainly those that foreshadow severe stock market corrections. But I still think that’s a ways away. Significant downturns are usually led by mini-corrections like the ones we are experiencing that produce lower highs and lower lows. But that’s not the case right now; in fact, the opposite is playing out. Stocks keep reaching higher highs and fail to dip below prior lows.

Most economists, including the Federal Reserve chairman, don’t see a U.S. recession until late 2019 or during the 2020 election year. Nevertheless, trouble overseas can migrate to American shores at any time – and that could be enough to push the U.S. into recession. And that’s when the shit really hits the fan.

Until then Plan Your Work and Work Your Plan – and keep those antacids close by because markets like this are certain to cause a prolonged case of agita.

Stay tuned…

![]()